ZERO EURO

Investment Guide

“The world of investing is one of the few human activities where YOU, by studying on your own for a couple of weeks, can do better than 99% of Professionals– cit. Mr. Rip

The Physics of Wealth

Chapter 1: The Physics of Wealth

Welcome. If you're here, you probably understand that how you manage money today will determine the quality of your life tomorrow. But perhaps there’s still a voice inside you whispering: "Investing is risky," or "Investing is for the wealthy," or worse yet, "Investing is like playing in a casino." I want you to take these beliefs and set them aside for a moment. We are about to enter a world that is not governed by luck, financial astrology, or the opinions of gurus on television. We are entering the world of Financial Physics.

There are immutable laws that govern the accumulation of wealth with the same ironclad precision with which gravity governs the movement of planets. If you drop an apple, propelled by gravity, it will fall downward. You don’t have to "hope" it happens. You know it will.

Similarly, if you spend less than you earn and invest the difference in productive assets (things that create value) for a sufficiently long time, you will build wealth. It is a mathematical principle, not a lottery ticket.

The problem is that most people try to violate these laws, searching for impossible shortcuts or stellar returns without risks. In this first Pillar, we will not talk about which stocks to buy. We will understand how to align your daily actions with these universal principles. True wealth is not just the final balance in your account: it is the ability to transform your work (potential energy) into freedom (kinetic energy). Let’s begin.

Chapter 2: The Farmer Metaphor

Imagine you are a Neolithic farmer.

Your job is simple but brutal: you must prepare the soil, plant the seeds, and wait.

Can you shout at the sky to make it rain? No.

Can you threaten the sun to shine more? No.

Can you pull the seedlings up to make them grow faster? If you do, you kill them.

The intelligent investor is exactly like that farmer.

There are variables that are under your control and variables that are NOT.

The fatal mistake made by 90% of losing investors is obsessively focusing on what they do NOT control: "What will the stock market do tomorrow?", "What will the Central Bank decide?", "Will there be a recession?".

No one knows. And worrying about it is an utterly wasteful use of mental energy.

The Investor-Farmer focuses only on what they control:

- Seeding (Savings): How much do you seed every month? If you don't seed anything, you won't reap anything, no matter how good the market is.

- The Soil (Asset Allocation): Where are you planting? On rock (money under the mattress), on sand (scams and Ponzi schemes) or on fertile ground (global stock market)?

- The Time (Time Horizon): Do you have the patience to wait for the harvest? Or do you run away at the first storm?

Wealth is a deferred harvest.

It is the reward the market pays to those who have the discipline to forgo a small pleasure today (spending all their salary) for immense freedom tomorrow.

Those who want to eat today the seeds that should become trees are doomed to future hunger.

In this journey, you won't need a genius IQ. You will need the stomach of a farmer and the patience of a monk.

Chapter 3: The Time Value of Money (TVM)

Let’s delve into the technical core of finance. The foundational concept of all modern economics is the Time Value of Money (TVM).

The textbook definition is: "A euro today is worth more than a euro tomorrow."

Why?

Many respond: "Because of inflation!" True, but that's not the only reason.

A euro today is worth more because it has Optionality. It has untapped potential.

Imagine holding an acorn in your hand.

Let’s say that acorn is worth 1 cent.

But if you plant it, in 20 years you will have an oak tree. And that oak tree will produce thousands of other acorns. And those acorns will grow into a forest.

So, how much is that acorn worth today? Is it worth just 1 cent, or is it worth the potential forest it holds?

In finance, money is that acorn.

Every time you spend €1,000 on a new iPhone that you don’t really need, we’re not saying you shouldn’t do it. But you need to be aware of what you are actually spending.

You are not spending €1,000. You are killing the future forest that those €1,000 could have generated if they had been invested at 7% per year for 30 years.

(Spoiler: €1,000 at 7% for 30 years becomes €7,600. That iPhone cost you nearly eight thousand future euros).

Understanding TVM means realizing that every euro spent today has an opportunity cost.

When you look at a €50 bill, you don’t just see a piece of paper to buy something. You see capital that, if invested today, can generate returns for the rest of your life.

Your task is to invest as much as possible instead of spending it all.

💰 Calcolatore TVM – Valore Temporale del Denaro

FV = PV × (1 + r)ⁿ – Quanto crescerà il tuo capitale?

Chapter 4: The Cost of Waiting (Workshop)

"I'll start investing next year when I get a raise." "I'll start when I've finished paying for the car." "Now is not the time; the markets are too high."

These are the most expensive lies we tell ourselves. In finance, time is not money. Time is Exponent. In the formula for compound interest, time is found in the exponent, not at the base. This means that a small delay at the beginning has devastating effects on the final outcome.

If you start investing €200 a month at 20 years old, by the age of 65 you will be a millionaire (with historical average returns of 7% per year). If you wait until you are 30 to start (just a 10-year delay), to reach the same final result you will need to invest almost double every month, for your entire life. Those 10 lost years cannot be recovered by putting in "a little more." They can only be recovered through an immense effort.

The simulator you find below is designed to help you "feel" this pain physically. Try entering your current capital. Then see what happens if you wait 5 or 10 years before investing it. The difference between the two final amounts is the cost of your procrastination. It is a tax you pay to yourself for your indecision. Face it. And then decide if it's worth starting today, even with a little. Because "a little" today is better than "a lot" tomorrow.

📉 Il Costo del Ritardo

Simula quanto perdi aspettando a iniziare.

Chapter 5: The Eighth Wonder of the World

It is said that Albert Einstein, when asked what the most powerful force in the universe was, replied: "Compound Interest. Those who understand it, earn it; those who don’t, pay it."

Whether this is a true or apocryphal quote, the concept is sacred.

Compound Interest is the reason why Warren Buffett is rich. Not because he is the best investor ever (he has achieved excellent returns, but others have done better in individual years). He is rich because he has been investing since he was 11 years old. He has harnessed compound interest for three-quarters of a century.

How does it work?

Imagine investing €100. In the first year, you earn 10%. You have €110.

In the second year, you earn another 10%. But you don’t earn €10 (which is 10% of 100). You earn €11 (which is 10% of 110).

That single extra euro is the interest on the interest.

It seems insignificant.

But project this mechanism over 30 or 40 years.

By the thirtieth year, the returns generated by your past interest will far exceed the money you put in yourself.

There comes a point, called the "Crossing Point," where your portfolio earns in one year more than you earn working.

At that moment, you are financially free. Your money works harder than you do.

The problem is that the human brain is not wired to comprehend exponential growth.

We are linear. 1, 2, 3, 4, 5.

Exponential is 1, 2, 4, 8, 16, 32, 64, 128...

The curve initially looks flat. It seems like nothing is happening. This is the so-called "Valley of Disillusionment."

Many give up here. They say, "I’ve been investing for 3 years and I’ve only earned a few hundred euros, it’s not worth it."

They quit just a moment before the curve starts to spike vertically toward the sky ("Hockey Stick").

The physics of wealth requires faith in mathematics, especially when the results are not yet visible.

Chapter 6: The Snowball Effect

Warren Buffett accumulated 99.7% of his wealth AFTER turning 52.

Read that sentence again.

If Buffett had retired at 60, no one would know who he is. He would have been a decent millionaire investor from Omaha, unknown to the world.

His secret was not "achieving astronomical returns" (though they were excellent, around 22% average annual), but rather "never stopping."

He started at 11 years old and never interrupted the chain of compound interest for 80 years.

This is the Snowball Effect.

Imagine you are at the top of a snowy mountain. You hold a small snowball the size of a fist. That snowball is your initial capital (maybe €5,000).

You start rolling it down.

After the first 10 meters, the ball is just a little bigger. You've collected only a few flakes of ice.

After 100 meters, it starts to be noticeably larger.

After 1 km, the ball has become an unstoppable avalanche that knocks down trees.

In that final phase, every single roll of the ball collects more snow than it gathered in the first 500 meters combined.

Your first 10 years of investing (from 25 to 35, or from 30 to 40) are only meant to build the ball. It is the hardest and most boring phase. You have to push it yourself. It seems like nothing is happening.

But if you persist, you will reach the phase where gravity takes over. Returns generate returns. The portfolio grows on its own by €10,000 or €20,000 in a single month, without you adding a single euro.

The goal of the game is to survive long enough to see the avalanche.

Chapter 7: Project Your Future (Lab)

It's easy to talk about "the long term" in abstract terms. It's much harder to visualize it concretely.

We live in the present. Our reptilian brain wants immediate rewards. The prefrontal cortex, which plans for the future, struggles to assert itself.

To help your prefrontal cortex win, you need to give it a clear picture.

Don't invest "to get rich." It's too vague.

Invest to:

- Be able to tell your boss to shove it in 15 years (Fuck You Money).

- Pay for your children's college without debt.

- Retire 10 years before the legal age and travel the world.

Use the simulator below to get a concrete idea. Think of it as a financial "time machine."

Enter how much you can realistically save and a cautious average return (e.g., 5-7% real). See where you could be in 20 or 30 years.

That final number represents the freedom you're buying, month by month.

Important note: time is the most critical factor. Extending your time horizon even by a couple of years often has a greater impact than slightly increasing your monthly contribution. Time is the most powerful leverage you have.

📈 Simulatore: Proietta il Tuo Futuro

Investimento iniziale + versamenti mensili con crescita composta.

Chapter 8: The Invisible Thief

There is a silent serial killer lurking in your bank account. It makes no noise. It leaves no traces. But every night, while you sleep, it enters your bank's vault and scrapes away a small piece of your coins. This killer is called Inflation.

Inflation is the general rise in prices, which results in the decrease of your money’s purchasing power. If you leave €100,000 idle in your bank account for 20 years, with an average inflation rate of 2-3% (historical), in the end, you'll still see "€100,000" on your statement. The bank hasn’t stolen anything from you. But when you go to the supermarket, you'll find that those €100,000 only buy half of what they did 20 years ago. You've lost 50% of your real purchasing power. It's as if the State had imposed a wealth tax of 50% without any law and without any protests in the streets.

Investing is not (just) a way to get rich. Investing is first and foremost Legitimate Defense. If you don’t invest, you are consciously choosing to lose money every day. Being "liquid" is not a zero-risk choice. It’s a choice of “certain loss.”

The only way to defeat the Invisible Thief is to make your money run faster than it does. You must invest in assets (stocks, real estate, bonds) that historically yield more than inflation. It’s not optional. It’s survival.

📉 Simulatore Inflazione: Il Ladro Invisibile

Scopri quanto vale davvero il tuo denaro tra N anni.

Chapter 9: Your Greatest Asset

When you think of your "portfolio," you probably think of your bank account and investment account.

But you are forgetting the greatest asset, worth millions of euros: YOURSELF.

In finance, this is called Human Capital.

It is the net present value of all the salaries you will earn from now until retirement.

If you are 25 years old and earn €30,000 a year, and you plan to work for 40 years with increasing salaries, your Human Capital may be worth (discounted) around 1 or 1.5 million euros.

This asset has very specific characteristics:

- It is similar to a Bond: it pays you a periodic coupon (salary) that is fairly secure (hopefully).

- It depletes over time: each year you work, you convert a part of Human Capital into Financial Capital. By age 65, your Human Capital is almost zero.

This perspective changes everything.

Since you already own a massive "bond" (millions!), when you are young you can and MUST afford to have very aggressive Financial Capital (100% Equity).

Because if the stock market crashes by 50% when you are 20, you have lost 50% of "very little" (your small savings), while your main asset (your job) remains intact. In fact, the crash is an opportunity to buy at a discount with your future salaries.

As you get older, Human Capital dries up and Financial Capital grows. At that point, you can no longer afford to lose 50%, because you no longer have time to recover through work. This is why bonds are added for protection.

Manage yourself like a business. Invest in your education to increase the return on your Human Capital. It is the investment with the highest ROI (Return on Investment) period.

👤 Il Tuo Capitale Umano

Quanto vali economicamente oggi? Il valore attuale dei tuoi stipendi futuri.

Chapter 10: Investment vs Speculation

We have reached the end of the first pillar. And before moving on, we need to clarify a fundamental distinction that will make the difference between success and failure in your financial journey.

We haven't talked about charts, P/E ratios, or dividends. We have spoken, I hope, to your mind and to your gut. Because before building a skyscraper, you must dig the foundations. And the distinction between investment and speculation is the deepest foundation of all.

Investment: The Patience Game

An investment is something that produces value over time, regardless of daily price fluctuations.

When you buy a global stock index, you are buying pieces of thousands of companies that sell products every day, generate profits, and reinvest them to grow. Whether you look at the price or not, whether the market is open or closed, those companies are working for you. Value accumulates day after day, like interest on a savings account, even if you don't see it.

The investor has a simple strategy:

- Buy productive assets (stocks, bonds)

- Hold them for decades

- Ignore market noise

- Reinvest dividends and coupons

- Reap the rewards of global economic growth

The investor knows they are playing a game where time is on their side. With each passing year, compound interest works for them. They are not in a hurry because they know that the final destination is guaranteed by the physics of wealth.

Speculation: The Timing Game

Speculation, on the other hand, is betting that the price of something will increase in the short term so that it can be sold to someone else.

When you buy Bitcoin hoping it will be worth double in a month, you are speculating. When you try to "time" the market by selling today to buy back tomorrow at a lower price, you are speculating. When you buy the stock of the week because "everyone is talking about it," you are speculating.

The speculator has a problem:

- They must get the timing right for buying

- They must get the timing right for selling

- They must outperform millions of professional traders

- They pay higher taxes (capital gains on short trades)

- They pay more commissions (for each buy and sell)

- They live in anxiety, checking prices every hour

The speculator plays against time. Every passing day, costs devour them. Every timing mistake can cost years of earnings. And statistically, 90% of speculators lose money in the long term.

The Ultimate Test

How do you know if you are investing or speculating? Ask yourself:

"If the market were to close for 10 years and you couldn't buy or sell anything, would you be happy owning this asset?"

If the answer is yes, you are investing. Companies will continue to produce value even if you cannot control the price. If the answer is no, you are speculating. Without the ability to sell quickly, your "investment" has no intrinsic value.

What We Want

This course is built to teach you to invest, not to speculate.

We want to:

- Buy and forget for decades

- Sleep peacefully during crises

- Accumulate wealth slowly but steadily

- Leverage time and compound interest as allies

- Pay as little tax as possible (hold long-term)

We do not want to:

- Watch charts every day

- Look for the "right moment" to enter

- Compete with professional traders

- Live in the anxiety of the next crash

- Burn money on commissions and taxes

The uncomfortable truth is that speculation is exciting. Investment is boring. But wealth is built with boredom, not with excitement.

If you want to get rich quickly, this is not the right place. But if you want to become rich for sure, stay.

Now that you have the mental foundations, you are ready to dive down the rabbit hole. In the next Pillar, we will face the number one enemy: Risk. And we will discover that it is not what you think. Welcome to the game of finance.

🧩 Verification Quiz: Pillar 1

Test yourself! Answer the 10 questions to verify your understanding.

1. What is the mathematical 'engine' of wealth growth?

2. Which variable has the strongest exponential impact in compound interest?

3. What does 'Human Capital' mean?

4. How does Human Capital behave over a lifetime?

5. What is the final goal of the investor according to the Lifecycle Theory?

6. If you double the annual return (e.g., from 5% to 10%), the final result after 30 years...

7. Why is it important to start investing as early as possible?

8. What is the number one enemy of savings sitting in a checking account?

9. The formula for future wealth depends on:

10. What happens if you withdraw interest every year instead of reinvesting?

Risk, Volatility and Resilience

Chapter 1: The Wall of Certainties

We live in a modern society obsessed with security.

We insure our car, home, health, smartphone, train trips. We seek the "stable job." We want contracts with guarantee clauses.

We have been taught to believe that risk is a failure of the system, a mistake to be avoided at all costs.

It is natural, then, that when an ordinary person approaches investments for the first time, their first question is:

"Is there something safe that yields well?"

I have bad news and good news for you.

The bad news is that that thing does not exist. It's a unicorn.

If someone offers you a "safe" investment with guaranteed returns above 5% (scam), run away.

The good news is that risk is not the monster you think it is.

Risk, in finance, is the raw material. It is the fuel.

Without risk, there is no return. If you want warmth, you have to burn wood. You cannot expect to warm yourself without lighting a fire.

In this pillar, we will learn not to avoid risk, but to tame it and use it to our advantage.

We will learn to distinguish "good" risk (the one that pays you) from "bad" risk (the one that destroys you).

Welcome to the world of profitable uncertainty.

Chapter 2: The Price of the Ticket

Why do stocks average a 7-8% return per year in the long term, while savings accounts or short-term government bonds yield 1% or 2%?

Why is the stock market so generous?

It isn’t. The market is not a charity, and it doesn’t give you anything for being nice.

That 7% is a compensation. It’s the "price" the market has to pay you to convince you to endure sleepless nights, alarming newspaper headlines, wars, pandemics, and sudden crashes.

Stock returns require an upfront payment: the acceptance of volatility.

Most people want returns but don’t want volatility.

They seek the "perfect timing" to enter and exit without pain, but this approach rarely works.

The return is the reward for your ability to withstand psychological fluctuations. If you are not willing to accept volatility, you will only get the yield of Postal Bonds (i.e., almost zero in real terms).

Accept volatility as part of the process. It is the price to pay for returns.

Chapter 3: Volatility Risk

This is, perhaps, the most important conceptual distinction of your entire journey.

In everyday language, the words "risk" and "volatility" are synonyms.

"That investment is volatile" means "It's dangerous."

In professional finance, these two terms describe completely different phenomena, even opposite in some respects.

Volatility is the fluctuation of prices in the short term. It is how much the price zigzags from today to tomorrow.

Volatility is like air turbulence. Is it annoying? Yes. Does it spill your coffee? Maybe. Does it make you feel nauseous? Often.

But turbulence is NOT the plane crashing.

If your portfolio declines by 2% today, have you lost money?

The correct answer is: NO. You have experienced a temporary fluctuation in the theoretical liquidation value.

As long as you don't sell, that loss is virtual. It's just information on the screen.

The true long-term investor does not look at the portfolio every day. In fact, they celebrate volatility. If you are in an accumulation phase with a Systematic Investment Plan (SIP), volatility is an advantage: by investing the same amount each month, when prices drop, you automatically buy more shares. It's like Dollar Cost Averaging: the market gives you a discount without you having to time it.

Chapter 4: The Definition of Risk

If volatility is just noise, what is true Risk then? Risk is the Permanent Loss of Capital. It’s when money disappears and never comes back. Game Over.

This happens in two main cases:

-

Asset Failure You buy the stock of a single company, like Parmalat or a meme crypto, and it fails. The value goes to zero. There is no recovery.

-

Panic Selling The market crashes by 30%, you can’t handle the stress or you need money suddenly, and you sell everything. At that exact moment, you have turned a temporary volatility into a permanent loss, crystallized and irreversible.

That’s why diversification is essential: it eliminates risk 1, the failure of the single asset. And that’s why having a liquid Emergency Fund is crucial: it eliminates or reduces risk 2, the need to sell.

But be careful, there is a crucial distinction you need to know:

-

Compensated or Systematic Risk This is the "good" risk. It’s the intrinsic market risk, such as buying the entire global index. You expose yourself to the uncertainty of the global economic future, and in exchange for this assumption of risk, the market "pays" you with a positive expected return in the long term. This is the risk that you want to take.

-

Uncompensated or Idiosyncratic Risk This is the "unnecessary" risk. It’s the specific risk you take on by betting on a single stock, a single industry like Tech, or a single country like Italy. Since this risk can be easily eliminated through diversification, the market owes you nothing for having taken it.

If you only buy Tesla stocks and Tesla fails, the market will not compensate you for your "courage." You could have diversified and didn’t. You took on uncompensated risk.

Your goal is to completely eliminate uncompensated risk by diversifying as much as possible, and to manage compensated risk well by choosing how much equity to have in your portfolio.

If you have eliminated these two risks, that is, single failure and forced selling, and cleaned your portfolio of uncompensated risks... the daily fluctuations can’t harm you. They are waves crashing on a rock. You are the rock.

Chapter 5: The Airplane Analogy

Imagine you have to fly from Rome to New York. Your goal is to reach your destination to start a new life (your financial freedom). You board the airplane (the global stock market). After an hour, the Captain announces: "Ladies and gentlemen, we are entering a zone of severe turbulence." The plane begins to shake violently. Luggage falls from the overhead compartments. The lights flicker. You are scared. It's natural.

In that moment, what do you do? Unbuckle your seatbelt, run to the emergency exit, open it, and throw yourself into the void without a parachute? Of course not. That would be suicide. You know that the turbulence is unpleasant, but the airplane is designed to withstand it. You know it will pass. Yet, in finance, that’s exactly what millions of investors do during a market crash. As soon as there is "turbulence" (the market drops 20%), they panic and jump out of the exit (sell everything and go to cash), crashing to the ground (permanent loss). If they had stayed seated with their seatbelts fastened (held), they would have arrived in New York a bit shaken but safe and sound.

Historical data is unequivocal: in over 100 years of history, a well-diversified global equity portfolio has NEVER gone to zero. It has always recovered from every world war, every pandemic, and every crisis. The only way to truly lose is to jump out of the airplane mid-flight. Stay seated.

Chapter 6: Volatility Lab

Now let's get our hands dirty with the numbers. Many people say, "I want an 8% return, but I don't want to see my portfolio drop more than 5%." It's like saying, "I want to become an Olympic marathon champion, but I don't want to sweat or get tired ever." Physics doesn't allow for that.

Use the simulator below. We have launched 50 Parallel Universes. Each of those gray lines is a possible future for your portfolio, based on the same premises, namely return and volatility.

What is Volatility? In finance, volatility is measured as the standard deviation of returns. In practice, it indicates how much returns fluctuate around the average. A volatility of 15% (typical of a well-diversified 100% global equity portfolio) means that in about 68% of cases, the annual return will be within the average ± 15%. For example, if the average return is 8%, you expect returns between -7% and +23% most of the time.

Try entering an 8% return and a 15% volatility. Do you see the chaos? The thick Blue line is the "Theoretical Average." It's the one they show you in brochures. Smooth, perfect, always rising. The gray lines are reality. Some will make you rich, others will make you suffer. The Red line is the worst-case scenario occurred in our 50 simulations.

You will notice that in the long term, let's say 15 or 20 years, most lines tend to rise nonetheless, driven by the power of compound returns. But the journey is never a straight line. Volatility is the price. Growth is the reward. You can't separate the two. Learn to love that jagged graph. It's the heartbeat of your wealth that's growing. A flat graph is a dead graph, just like money under the mattress.

📊 Simulatore Volatilità

Visualizza come media e deviazione standard creano percorsi reali diversi.

Chapter 7: The Cruel Asymmetry

There is one true mathematical reason to be cautious and not take excessive risks, avoiding going "all-in": the Asymmetry of Losses.

Gains and losses in percentage terms are not equal.

Our intuitive brain thinks: "If I lose 50%, then I just need to gain +50% to break even."

FATAL ERROR.

Let's do the math:

You have €100. You lose 50%. You are left with €50.

Now, to get back to €100 starting from €50, you need to gain another €50.

But €50 on a base of €50 represents a gain of 100%!

You have to double your capital just to return to square one. And doubling capital is difficult; it takes time and risks.

If you lose 90%, as happened to many tech stocks during the dot-com bubble, to break even you need to achieve +900%. You need to do an "x10." It’s almost impossible.

This law explains why Warren Buffett's first rule is "Don't lose money" (I mean permanent/deep losses).

A drawdown, or peak-to-trough decline, of 10% or 20% is normal and can be easily recovered with a +12% or +25% return.

A drawdown of 50% or 60% is a chasm that may take a decade to fill.

That’s why portfolios are built with a portion of "buffers," such as bonds, gold, or cash: to avoid a decline that becomes so deep that recovery in a human timeframe becomes mathematically impossible.

To engrave the concept of asymmetry in your mind, use the calculator below.

Enter a percentage loss, the so-called Drawdown, and observe the "Required Recovery" column.

Notice that up to 15-20%, the two figures are similar. The damage is manageable.

But exceed the threshold of 30-40% and you will see the curve spike vertically.

At -50%, the recovery requirement doubles.

At -75%, the requirement quadruples.

This graph and the numbers you see should terrify you. They are designed that way.

They should teach you that the real enemy is not "not earning enough," but "digging a hole too deep."

A portfolio that shows +50% one year and -50% the next appears to have an average return of 0%, right? WRONG. Look at the concrete numbers: start from €100, rise to €150 (+50%), then drop to €75 (-50% of €150). Final result: you’ve lost 25% even though "the average" was zero. This is why real compounded return matters, not simple arithmetic average.

Stability, or reducing drawdowns, is the secret to maximizing the final compounded return or CAGR (Compound Annual Growth Rate).

"Slow and steady wins the race." In finance, this is literally true: those who avoid major crashes outperform those who make big gains followed by big disasters.

⚡ Calcolatore del Baratro – Asimmetria delle Perdite

Scopri quanto devi guadagnare per recuperare da una perdita.

| Perdita | Recupero Necessario |

|---|---|

| -10% | +11.1% |

| -20% | +25.0% |

| -30% | +42.9% |

| -40% | +66.7% |

| -50% | +100.0% |

| -60% | +150.0% |

| -70% | +233.3% |

| -80% | +400.0% |

| -90% | +900.0% |

Chapter 8: The Only Free Lunch

In the world of economics, there is an unwritten law: "There are no free lunches." If you want higher returns, you must take on more risk. It’s the currency of exchange. However, there is a single mathematical exception to this rule. Nobel laureate Harry Markowitz called it "the only free lunch in finance."

It’s called Diversification.

The Magic of Correlation

Imagine selling swimsuits. If it rains, you earn nothing. High risk. Now imagine having a friend who sells umbrellas. If it’s sunny, he earns nothing. When you partner up, magic happens: you always earn. When it rains, you sell umbrellas. When it’s sunny, you sell swimsuits. The average return remains the same, but volatility (the risk of making zero revenue) drastically collapses.

Don’t Put All Your Eggs in One Basket

This old adage is supported by more sophisticated mathematics. Adding uncorrelated assets (that don’t move together) to your portfolio reduces overall risk WITHOUT necessarily reducing expected returns.

Investing in a single asset class? Risky. Investing in a mix of different assets that behave differently? You’re building an unsinkable ship. Because when one engine falters, the other often speeds up. Diversification is the insurance you get paid by the market, instead of paying for it yourself. It’s the only way to sleep soundly while your money works.

Chapter 9: Know Thyself

There is no "Perfect Portfolio" in absolute terms. There is only the perfect portfolio for you.

To find it, you need to solve an equation with two personal variables:

-

Risk Capacity: This is an objective, financial fact.

How much money can you afford to lose without your life changing?

If you’re a 25-year-old living with your parents, have a stable job, and are investing money you won’t need for 30 years, your risk capacity is VERY HIGH. Even if you lose 50%, you won’t end up on the street. You have time to recover.

If you’re a 60-year-old nearing retirement with little savings, your capacity is LOW. A downturn might force you to forego medical care or sell your home. -

Risk Tolerance: This is a subjective, psychological fact.

How do you react when you see red?

Do you sleep at night? Do you get gastritis? Do you argue with your spouse? Do you check the banking app every 5 minutes in a panic?

There are wealthy 20-year-olds (high capacity) who panic over a -5% (low tolerance).

There are zen 60-year-olds (low capacity) who wouldn’t bat an eye at a -30% (high tolerance).

The classic mistake is to look only at the numbers (Capacity) and ignore the emotions (Tolerance).

Many advisors tell you: "You're young, put everything in stocks!"

Mathematically correct. But if you then sell everything at the first downturn out of fear, that advice has ruined you.

The best portfolio is the one you can hold onto (Hold) even in the worst days.

In the lab below, you'll find an interactive questionnaire that will help you understand your personal risk profile, combining both your objective capacity and your psychological tolerance. There are no right or wrong answers: only honest answers.

Chapter 10: The Golden Rule

Here is the final formula for determining your risk profile.

The risk you should assume must be the LOWER of your Capacity and your Tolerance.

Risk Assumable = Min(Capacity, Tolerance)

Example 1: Young (High Capacity) but anxious (Low Tolerance).

You should invest prudently (e.g., 40% stocks, 60% bonds). Of course, you will forgo some potential returns (opportunity cost), but you will avoid the catastrophic risk of selling everything in panic (panic selling). A mediocre return is better than a capital loss.

Example 2: Elderly (Low Capacity) but reckless (High Tolerance).

You must invest wisely! Even if you feel like Rambo and are not afraid of anything, if you lose your pension money, you are ruined. Math triumphs over courage.

Only when both Capacity and Tolerance are HIGH can you afford aggressive portfolios (100% stocks).

Your task from now on is to work on both variables:

- Increase your Capacity by saving and creating an Emergency Fund.

- Increase your Tolerance by studying (knowledge dispels fear) and getting used to volatility.

Only then can you afford more "engine" and less "brake" portfolios, and accelerate toward wealth.

But don’t cheat. If you respect your limits, you will arrive safe and sound. If you ignore them, a crash is guaranteed.

🧩 Verification Quiz: Pillar 2

Test yourself! Answer the 10 questions to verify your understanding.

1. What does Volatility measure in finance?

2. What is 'Drawdown' risk?

3. If you lose 50%, how much do you need to gain to break even?

4. What is 'Risk Capacity'?

5. What is 'Risk Tolerance'?

6. Is saving money under the mattress risk-free?

7. Which asset class has historically the highest risk/volatility?

8. Volatility in the long term is:

9. What does 'Risk Adjusted Return' mean?

10. Can 'Idiosyncratic' risk (of a single company) be eliminated?

Financial Markets

Chapter 1: The Great Theater of Finance

"The stock market is the only store in the world where customers run away when there are sales."

Imagine entering an immense global market, a bazaar that never closes, where billions of euros change hands every day in the blink of an eye. This is not a casino, although many treat it as such. It is the pulsating engine of the global economy, the mechanism through which humanity finances its progress. Welcome to the Financial Markets.

The financial world offers a vast and complex arsenal of instruments. In this pillar, we will explore all types of assets available in the market, from the simplest stocks to the most complex derivatives, from safe bonds to speculative cryptocurrencies. But to navigate this apparent chaos, you must understand a single, fundamental truth.

When a company or a state needs money to grow, it has only two fundamental paths available.

The first is to take out a loan, meaning to create Debt. The company says: "Lend me some money, and I will pay you back with interest." This is the realm of Bonds, where the keyword is safety and stability.

The second is to give away a piece of itself, meaning to offer Equity. The company says: "Give me money, and you will become my partner. If I do well, you earn with me. If I fail, you lose with me." This is the vibrant world of Stocks, where the risk is higher but the rewards can be unlimited.

Everything else, such as derivatives, options, futures, crypto, and commodities, is built on this foundation or represents more complex and risky variations of these two primordial concepts.

In this pillar, we will not just list definitions. We will analyze in detail how Stocks work, distinguishing between different types and understanding what truly drives their prices. We will then move on to the world of Bonds, discovering how government and corporate securities can protect your capital.

We will also venture into the more complex territories of Derivatives, such as options and futures, and into the new digital world of Cryptocurrencies, before touching on alternative assets like Commodities and REITs.

Finally, we will tie everything together by understanding Market Mechanics, discovering how correlation and diversification are the true secret weapons of the smart investor.

Note: ETFs, which are the ideal container for these instruments, will be the stars of the next pillar. Here we focus on the "bricks" that compose them.

By the end of this pillar, the market will no longer be a mysterious enemy to conquer or a beast to tame. You will see it for what it truly is: a tool. A powerful, complex, sometimes frightening tool, but absolutely essential for anyone looking to build lasting wealth.

History teaches us that there is no return without risk. But it also teaches us that risk, when understood and managed, is the price of the ticket to financial freedom.

Are you ready to become a true capitalist? Let's begin.

Chapter 2: Stocks - Become the Master

Buying a stock does not mean betting on a red or green number flashing on a screen. It means buying a piece of a real business. It means becoming an owner.

When you buy a share of Apple, you are not buying a "tech stock." You are buying the patents of the iPhone, the glass stores in Manhattan, the minds of engineers in Cupertino, and a portion of the future earnings that will be generated from every app sold. You are a partner of Tim Cook, even if you own just one-millionth of the company.

What It Means to Own Stocks

Stock ownership gives you the right to the profits of the company, often distributed in the form of dividends. It’s money working for you while you sleep, a share of the profits generated by the business.

But why do stocks go up? In the short term, prices are slaves to emotion: news, fears, greed, and impulsive tweets can swing quotes relentlessly. But in the long term, the price of a stock follows a single guiding star: Profits.

If a company sells more products, becomes more efficient, and earns more year after year, its value must rise. It’s an economic law of gravitation. The global stock market is, ultimately, a bet on human ingenuity and our ability to solve problems and create value. This is why investing in stocks is the only way to truly participate in the creation of global wealth, historically outpacing inflation.

The Stock Arsenal

Not all stocks are created equal. The market offers different types of securities, each with its own characteristics.

Companies are classified primarily by Size or Market Capitalization. This ranges from gigantic Large-Cap (like Apple and Microsoft), mature and stable, to Small-Cap, smaller, agile companies with explosive growth potential but a much higher likelihood of failure. There are also Micro-Cap stocks, extremely volatile and risky, often a playground for speculation.

Another major division is between Growth and Value. Growth stocks belong to rapidly expanding companies (often in tech: think Tesla or Nvidia) that reinvest all their profits to grow even more, often resulting in volatility and high prices relative to current earnings. Value stocks, on the other hand, are solid, often undervalued companies that pay regular dividends and offer greater stability.

Finally, let's not forget geography. You can invest in Domestic companies (Italy/Europe), in Developed Countries (USA, Japan, etc.), or venture into Emerging Markets (China, India, Brazil), accepting greater volatility in exchange for access to rapidly growing economies.

Chapter 3: The Engine of Growth

We've said that volatility is the price to pay. But for what? Why should you endure these roller coasters? Because, in the long run, the stock market rises?

It’s not magic and it’s not luck. There’s a powerful engine that pushes prices upward, made up of three fundamental cylinders.

Human Ingenuity and Innovation

When you invest in a global index, you’re not buying "paper." You're funding millions of people who wake up every morning with a goal: to do things better than yesterday. Finding a cure for a disease, inventing a faster smartphone, transporting goods more efficiently, building safer homes. This relentless drive for improvement creates value. And that value translates into economic growth. You are betting on humanity's ability to solve problems.

Reinvested Earnings

Companies don’t just cash in profits and stash them away. A portion of those profits is paid out to you (dividends), but a huge part is reinvested. The company uses its earnings to buy new machinery, hire better talent, open new branches, or conduct research. This compounded reinvestment ensures that the company itself becomes larger and more productive year after year. It’s like a tree that uses its fallen leaves to nourish its roots and grow even taller.

Protection from Inflation

Stocks are "pieces of real businesses." If there’s inflation and the price of bread doubles, the baker will collect double. Companies have the power to raise the prices of their products to keep up with inflation. Unlike bonds or cash, which are eaten away by inflation, stocks tend to float above it, preserving your real purchasing power.

Don't invest to "make easy money." Invest to participate in the creation of humanity's wealth. Volatility is just the background noise of this engine running. Sometimes it coughs, sometimes it accelerates, but the long-term direction is given by our evolution. As long as you believe that tomorrow people will want to live better than today, you have a reason to be invested.

Chapter 4: Bonds - Debt is Security

While stocks make you an owner, Bonds make you a banker. A bond is, in its purest essence, a loan. When the State or a company needs liquidity, rather than knocking on a bank's door, it turns to the market by issuing a security that promises two things: the return of the lent capital by a certain date (maturity) and the payment of periodic interest (coupon) as a thank you for the trust.

Why Buy Debt?

The answer is simple: certainty. In a financial world dominated by uncertainty, knowing exactly how much you will earn and when is a luxury that has invaluable worth. Bonds serve two vital functions in your portfolio.

The first is to generate income: the coupons are regular cash flows that you can use to live or reinvest. The second, and perhaps more important, is to act as a buffer. Often, when stocks crash due to fears of a recession, bonds tend to remain stable or even rise, acting like the airbag in your car: they won’t make you go faster, but they will save your life in case of an accident.

A World of Debts

Not all debts are equal. The bond market is vast and diverse, primarily categorizable by issuer and structure.

Government Bonds (such as Italian BTPs or US Treasuries) are issued by governments. They are generally considered the safest investment possible because a government has the power to tax its citizens or print money to honor its debts. For this reason, they typically offer lower yields. In Italy, the yields from qualified government bonds benefit from a reduced tax rate of 12.5% instead of the 26% applied to stocks and equity ETFs.

Corporate Bonds, on the other hand, are issued by companies. Here the risk is higher — a company can default much more easily than a government — and consequently, the yields offered are higher. Rating agencies help us navigate this sea, assessing both states and companies and distinguishing between solid "Investment Grade" issuers (like Apple, Microsoft, or stable states like the USA and Germany) and riskier "High-Yield" or "Junk" issuers, which promise stellar returns in exchange for a real default risk.

Along with the issuer, the structure also varies. Most bonds pay a fixed coupon, simple and predictable. Others, known as Zero-Coupon bonds, pay nothing during the life of the loan but are sold at a significant discount to the redemption value. There are also variable-rate bonds, which protect you if rates rise, and inflation-indexed bonds (such as Italian BTP Italia for Italian inflation, BTP€i for European inflation, or US TIPS), specifically designed to defend your purchasing power from monetary erosion.

The Time Factor

Finally, there is the duration. Short-term bonds (under 3 years) are almost akin to cash: low volatility and very safe. Long-term bonds (over 10 years) offer higher yields to compensate for the prolonged commitment, but as we will see in the next chapter, they carry a sneaky risk related to interest rates. The golden rule is that the longer the maturity, the higher the yield, but also the greater the price volatility.

Chapter 5: The Dark Side (Interest Rate Risk and Duration)

Many investors fall into the trap of believing that bonds cannot lose value. It’s a mistake that can be costly. It’s true that if you hold a bond until maturity and the issuer doesn’t default, you’ll get your capital back. But what happens if you need to sell before then?

This is where the public enemy number one of bonds comes into play: Interest Rates.

The Iron Law

There exists a mechanical inverse relationship, almost a physical law of finance: if rates rise, the price of bonds falls.

To understand why, imagine you own an old bond that pays 1%. Suddenly, market rates rise, and new bonds identical to yours are issued but pay 1.5%. Who would ever want to buy your old bond at 1%? No one, unless you "sell it off" at a lower price, thus compensating for the lower yield with a gain on the purchase price. That fire sale is, technically, the capital loss you see in your portfolio.

Duration: The Risk Multiplier

The sensitivity of a bond to this phenomenon is measured by Duration. Although it is expressed in years, you should think of it as a risk multiplier.

Rule: A bond with a duration of 10 years will lose about 10% of its value for every 1% increase in rates.

That’s exactly what happened in 2022 when "safe" long-term bonds lost 30-40% of their value because rates went from zero to over 4% in no time. The year 2022 was a unique event: the fastest and most violent rate hike of the last decades, imposed by central banks to curb post-COVID inflation. The lesson is brutal but clear: extending the maturity to seek a few extra basis points of yield transforms your "airbag" into another source of danger.

The Other Monsters

Beyond rates, the bond investor must be wary of other risks.

The most obvious is Default Risk, which is the possibility that the issuer will not repay the debt. This is rare for government bonds from developed countries but real for corporate bonds or those from emerging markets. There’s also Inflation Risk: if inflation is running at 5% and your bond yields 2%, in real terms you are becoming poorer with each passing day.

Finally, don’t forget about Currency Risk. Buying a U.S. Treasury bond may seem safe, but if the dollar loses 10% against the euro, your loss on the exchange rate could erase years of coupon payments.

The truth is that bonds are not "safe" in an absolute sense. They are "safer" than stocks because they are less volatile and offer certain cash flows, but they still require understanding and respect.

Chapter 6: Bond Ladder vs ETF

Now that we understand the risks (Rates and Duration), a practical question arises: how do I buy these bonds? You have two main paths. And the choice once again depends on your objective.

1. The Sniper: The Bond Ladder

The "Bond Ladder" approach involves buying individual bonds with different maturities and holding them until maturity. For example: You buy a BTP maturing in 2026, one in 2027, one in 2028, and so on.

The magic advantage: If you hold the bond until maturity, you ignore price volatility. Rates go up? The price of your bond drops on paper? You don't care. You know that in 2027 you will receive exactly your €100 + the coupons. You are "immunizing" the interest rate risk for that specific date. It's ideal for planned expenses.

2. The Conveyor Belt: The Bond ETF

The bond ETF is a fund that buys hundreds of bonds for you. But beware: to maintain a constant duration (e.g., 7-10 years), the ETF never holds the securities to maturity. It sells the bonds that are about to mature and buys new longer ones. It's an infinite conveyor belt.

The problem: Since there is never a "final maturity," you are always exposed to interest rate risk. If rates rise (as in 2022), the ETF loses value and you do not have the guarantee of recouping your capital at a specific date. However, the ETF immediately starts buying new bonds that yield more. So your future yield increases.

Chapter 7: Derivatives - Options and Futures

Note: This chapter is designed to enhance your financial literacy. Derivatives are complex instruments, often double-edged swords, typically reserved for professionals and experienced traders.

Beyond Ownership and Debt

If stocks and bonds are the building blocks of the economy, derivatives are the bets made on those blocks. As the name suggests, they are instruments whose value "derives" from something else: a stock, an index, a commodity, or an interest rate.

Options are contracts that give you the right—but not the obligation—to buy or sell an asset at a predetermined price (Strike Price) by a certain date. To have this privilege, you pay an immediate cost called Premium.

- Call (Bullish): You bet that the price will rise. If the market price exceeds the Strike Price, you earn the difference. Your maximum risk is limited to the Premium paid, while your potential gain is theoretically unlimited (see green chart below).

- Put (Bearish/Protection): You bet that the price will fall. If the price crashes below the Strike Price, the value of your option increases, offsetting losses in your stock portfolio. It's like insurance: you pay a premium upfront to be covered in case of disaster (see red chart below).

Futures, on the other hand, are binding contracts. Here you commit to buying or selling the asset at a future date. They were created to allow farmers to lock in the price of wheat before harvest, eliminating uncertainty, but today they are heavily used by speculators exploiting leverage. Leverage is the superpower (and curse) of derivatives: it allows you to move large amounts of capital by investing small sums, magnifying gains but also losses that can exceed the invested capital.

For the passive investor building wealth over the long term, these instruments are rarely necessary. They add complexity, costs, and risks that often do not justify the benefits. However, knowing they exist and how they work is essential to understanding the full architecture of financial markets.

Chapter 8: Cryptocurrencies - The New Digital World

Note: Cryptocurrencies do not have a long history behind them, and their future behavior is still a topic of debate. Currently, they are speculative assets with extreme volatility.

Beyond Traditional Currency

Cryptocurrencies are not just digital coins; they are attempts to reinvent the very concept of money and finance using cryptography and blockchain technology. At the core of it all is the idea of decentralization: a system where no central bank or government has the power to print money or censor transactions.

The undisputed king is Bitcoin, often referred to as "digital gold." Launched in 2009, it introduced the concept of absolute digital scarcity: there will never be more than 21 million coins. It has become a speculative store of value for those fearful of fiat currency devaluation. Then there is Ethereum, which goes beyond mere currency: it is a programmable platform on which decentralized applications and smart contracts are built.

There are thousands of other cryptocurrencies ("altcoins"), but the vast majority are experimental projects, worthless memes, or, worse, scams.

Risks and Realities

For an investor, cryptocurrencies represent a double-edged sword. On one hand, they offer the possibility of astronomical returns, on the other, they come with extreme volatility: losing 50% or 80% of value in a matter of weeks is almost the norm, not the exception.

The fundamental problem is that they generate nothing: there are no earnings, no dividends, no coupons. The only way to profit is to find someone else willing to buy them at a higher price than yours. It's the classic "house of cards" of financial theory.

This makes them purely speculative assets. They can have a place in a well-diversified portfolio as a bet on the future of blockchain technology, but allocating a significant percentage of one’s wealth to cryptocurrencies is gambling, not investing. Additionally, they carry unique technological risks: losing private keys means losing your funds forever, with no customer service hotline to call.

For the passive investor looking to build wealth over the long term, cryptocurrencies are not necessary. If you choose to include them, they should occupy only a tiny part of the portfolio.

Chapter 9: Other Assets - Beyond the Ordinary

Beyond the classic stocks-bonds duo, the financial world offers a myriad of alternative assets. While they are often not essential for a solid portfolio, knowing them helps you better understand the options available to you.

Commodities: The Raw Materials

Commodities are the physical bricks of the economy: oil, gas, grain, metals. Unlike stocks, they do not produce cash flows; their value depends purely on scarcity and demand.

Gold deserves a separate discussion. For millennia, it has been considered the ultimate safe haven, a protection against inflation and systemic crises. However, it is a non-productive asset: a gold bar in a safe will remain unchanged in a hundred years, generating not a single cent in profit. It should be viewed more as insurance than as an investment.

Other commodities, such as oil or agricultural products (the famous orange juice from the movie "Trading Places"!), are extremely volatile and complex, influenced by unpredictable factors like weather, geopolitics, or wars. For the average investor, they often do not justify the risk.

Real Estate on the Stock Market: REITs

Many love real estate but hate management (tenants, maintenance, taxes). REITs (Real Estate Investment Trusts) are often presented as the solution: publicly traded companies that own properties and distribute profits.

However, it is crucial to understand a critical difference: REITs are stocks, not real estate. When you buy a physical apartment, the price does not fluctuate every second. When you buy a REIT, you are purchasing a stock that behaves like one. It has the volatility of the market, suffers from interest rate increases, and can lose 30-40% in a year, just like shares of Apple or Google. Don't think that having REITs in your portfolio equates to having "the safe brick." It is exposure to the real estate sector, but with the dynamics (and risks) of the stock market.

Advanced Speculative Instruments

Finally, there are purely speculative instruments such as Forex (currencies) and CFDs (Contracts for Difference). Here we enter the territory of professional trading, often characterized by the use of leverage: a mechanism that amplifies both gains and losses, potentially wiping out your capital in minutes.

Private Equity and Hedge Funds also fall under alternative assets, but they are generally reserved for institutional or very wealthy investors, with high costs and entry barriers that rarely justify the benefits for small savers.

The truth is that to build solid wealth, there is no need to complicate your life with exotic instruments. A well-diversified portfolio of stocks and bonds is more than sufficient to achieve any financial goal.

Chapter 10: The Art of Correlation

We have seen how stocks and bonds work. But the real secret to building a solid portfolio lies not in choosing individual assets, but in understanding how they perform together. This is called correlation.

The Mathematics of Diversification

Correlation simply measures how closely two assets tend to move together. If you own two stocks that rise and fall in unison (high correlation), you have diversified nothing: you have merely doubled your bet. True security arises when you combine assets that "ignore" each other or, better yet, move in opposite directions.

Imagine a portfolio made up solely of technology stocks. If the sector crashes, your wealth crashes. But if you add government bonds, something interesting happens. Historically, when the stock market panics (recessions, crises), investors sell stocks and rush towards the safety of government bonds. This drives up the value of bonds just as stocks decline.

The Perfect Pair

This is the secret of the classic balanced portfolio (often referred to as 60/40): when one part suffers, the other often thrives, or at least cushions the blow.

If the stock market plummets by 50%, a 100% equity investor sees their capital halved. But someone with 40% in bonds (which may rise by 10% due to the flight to safety) will experience a much smaller loss, perhaps 25%. You have reduced the pain by half, allowing you to stay invested and not sell at the worst moment.

Of course, diversification has a cost: when stocks soar, bonds act as a drag, slightly reducing the overall gain. Stocks bring growth. Bonds bring stability. Together, they create a portfolio stronger than the sum of its parts. And there are rare and unfortunate years (like 2022) when everything declines together because inflation hits everywhere. But in the long game of decades, diversification remains the only "free lunch" in finance: it dramatically reduces risk at the cost of only a small fraction of potential returns.

Now that you understand assets and how they work together through correlation, you are ready to discover the tool that makes all this accessible with just one click: the ETF.

🧩 Verification Quiz: Pillar 3

Test yourself! Answer the 10 questions to verify your understanding.

1. What distinguishes Stocks from Bonds?

2. What is the main risk of fixed-rate Bonds?

3. In a risk/return hierarchy, which order is correct?

4. What happens in a 'Bear' market?

5. What is Correlation risk?

6. Are derivatives (Options/Futures) recommended for the average investor?

7. Bitcoin is considered:

8. Geographic diversification serves to:

9. A bond with high Duration is:

10. The correlation between Stocks and Safe Government Bonds is typically:

The ETF Revolution

Chapter 1: The Democratic Revolution

In 1993, an invention changed finance forever: SPY (SPDR S&P 500 ETF Trust) was born.

Before ETFs, if you wanted to invest in the stock market, you had two painful paths:

Stock Picking:

You had to buy individual stocks (expensive, risky, and difficult).

Active Mutual Funds:

You had to give your money to a bank, pay ridiculous entry fees (3-4%) and insane annual management costs (2-3%), only to achieve returns that were almost always below the market.

The rational choice explained in 2 seconds.

The ETF (Exchange Traded Fund) shattered this oligopoly.

An ETF is a "basket" of securities that has two revolutionary features:

It’s a Fund:

It allows you to buy 500 or 3,000 companies with a single click (instant diversification).

It’s Exchange Traded:

It buys and sells like a stock, in real-time, during market hours. You don’t have to wait for the end-of-day NAV like in mutual funds.

It’s total democratization. Today, with €50, you can buy a piece of the entire world, paying ridiculous fees (0.07% - 0.20% per year).

For banks, it was a disaster (they lost their hefty fees). For you, it was salvation.

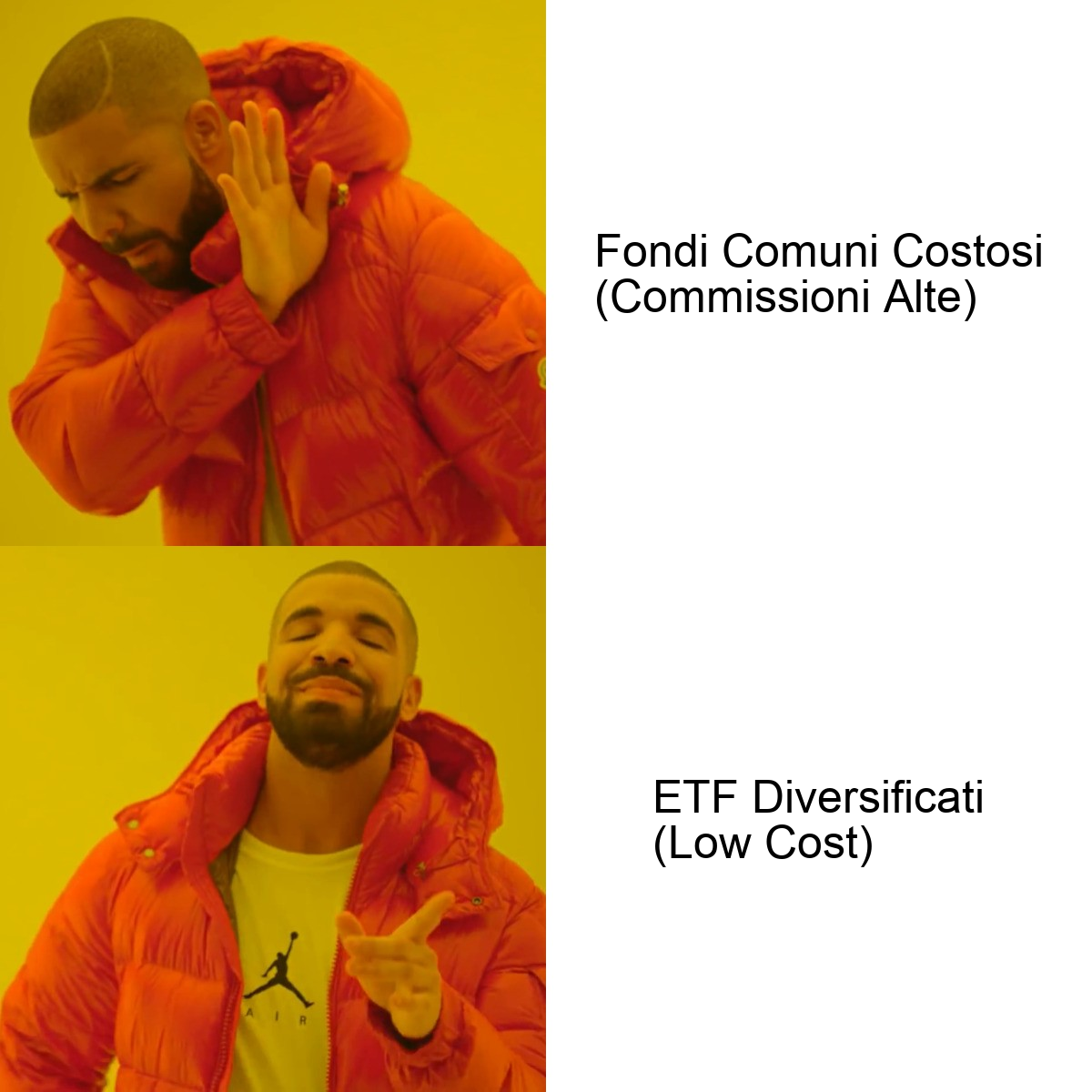

Why Passive Management Beats Active Management

The ETF follows a passive management philosophy: it simply replicates an index (e.g., S&P 500) without trying to beat it.

Traditional mutual funds follow an active management approach: a manager tries to select the "best" stocks to outperform the market.

Burton Malkiel, in his book "A Random Walk Down Wall Street," demonstrated that over 90% of active managers underperform the index in the long run (10-20 years).

Why?

Costs Erode Returns:

If an active fund costs 2% per year and the passive ETF is 0.15%, that manager must beat the market by at least 2% just to break even. Year after year, it’s mathematically impossible for the majority.

Luck Doesn’t Last:

Some managers "beat" the market for a few years, but most do so by luck, not skill. In the long run, luck evaporates, and the costs remain.

Market Efficiency:

Stock prices already incorporate all available information. "Beating the market" means being smarter than millions of other investors. Is it possible? Rarely.

Conclusion: Passive management doesn’t aim to be the best. It seeks to be average (the market), but with extremely low costs. And this, in the long run, beats almost everyone.

Chapter 2: The ETP Family (ETF, ETC, ETN)

We often use the word "ETF" to refer to everything, but technically we are talking about ETP (Exchange Traded Products).

It is essential to understand the legal differences, as they change the risk.

The ETP family has three members:

ETF (Exchange Traded Fund)

It is a collective investment scheme.

The key feature is Asset Segregation. The fund's money is separated from that of the issuer (e.g., BlackRock or Vanguard).

If BlackRock fails, your money is NOT affected by BlackRock's creditors. It belongs to you. It is the safest instrument.

ETC (Exchange Traded Commodities)

These are used to invest in single commodities (Gold, Oil, Wheat).

By law, an ETF must be diversified, so there cannot be a "Physical Gold ETF." The ETC is used instead.

Important Note: If an ETP invests in multiple different commodities simultaneously (e.g., a basket of gold, silver, oil), then by law it is classified as an ETF, not an ETC. ETCs invest in single commodities.

ETN (Exchange Traded Notes)

Used for exotic things (Cryptocurrencies, complex leveraged investments, volatility).

It is a bank debt security. Here lies the Issuer Risk. If the bank that issued the ETN goes bankrupt, you become a creditor and may lose your money (as happened with Lehman Brothers).

Rule: Whenever possible, always choose ETFs. Use ETCs only for commodities. Avoid ETNs unless you know exactly what you are doing.

Chapter 3: Replication (Physical vs Synthetic)

How does the ETF track the index?

There are two main methods of Replication. You need to distinguish them by reading the KIID.

Physical Replication

The ETF physically buys the stocks of the index.

- Full Replication: Buys ALL 500 stocks of the S&P 500. Perfect, but expensive if the index has 3,000 illiquid stocks.

- Sampling: The issuer buys only a representative subset of the stocks in the index. Efficient.

Advantage: Total transparency. No counterparty risk.

Synthetic Replication (Swap-based)

The ETF does not buy the stocks of the index.

It enters into a contract (Swap) with an investment bank (Counterparty).

The ETF provides the bank with a collateral basket (e.g., government bonds) and the bank commits to paying the exact return of the index (e.g., S&P 500) minus the cost of the swap.

Advantage: Absolute precision (almost zero Tracking Error) and tax benefits on certain dividends. In particular, on US stocks, European investors save about 15% in Withholding Tax on dividends that are normally withheld at source (the US withholds 15% on dividends paid to foreigners, but synthetic replication sidesteps this issue).

Disadvantage: Counterparty Risk. If the bank fails, you could lose a small part of the value (legally limited to 10%, but often entirely offset by the collateral).

Historical Note: It is important to emphasize that currently no UCITS ETF with synthetic replication has ever failed. However, in 2008 several banks failed (a real counterparty risk), so it is fair to assess this risk, even though it is mitigated by collateral.

For the average investor, Physical Replication is preferable for peace of mind.

However, for S&P 500 ETFs, Synthetic has historically yielded more due to savings on US taxes.

Chapter 4: Accumulation vs Distribution

Each ETF has a dividend policy. You must choose the right one for your tax objective.

Distribution (Dist) The ETF collects dividends from companies and deposits them into your account (quarterly or semi-annually). Pro: Cash flow, psychological motivation. Con: Tax Inefficiency. In Italy, every time you receive a dividend you immediately pay 26% in taxes. That money disappears and does not generate compound interest. Code: They often end with "Dist" or "D".

Accumulation (Acc) The ETF collects dividends and automatically reinvests them by buying more shares of the fund itself. You do not see deposits. The value of your shares increases faster. Pro: Maximum Tax Efficiency. You do not pay taxes on dividends until you sell the ETF (maybe in 20 years). Compound interest works on gross, not net. It's a huge mathematical advantage called "Tax Deferral." Additionally, synthetic replication ETFs offer an extra benefit by avoiding Withholding Tax on foreign dividends (e.g., US stocks: you save the 15% withheld at source). Con: No immediate cash flow. Code: They often end with "Acc" or "C".

Advice for Italians: During the wealth-building phase (Accumulation), ALWAYS choose Accumulation ETFs. Don’t give 26% to the State every year. Pay it only at the end. In the subsequent chapters, we will understand why dividends are irrelevant.

Distribution vs Accumulation: The Real Comparison

Even if you need periodic liquidity, it’s more efficient to sell only the necessary shares of an accumulation ETF rather than receive dividends taxed at 26% every year.

Practical Example: Invest €10,000 in a global equity ETF for 20 years, with an annual return of 7% (of which 2% is from dividends and 5% from price growth).

Distribution ETF:

- Each year you receive about €200 in dividends (2% of initial €10,000, increasing).

- You immediately pay 26% tax on this = €52 lost.

- You reinvest only €148 net.

- After 20 years: ~€25,000.

Accumulation ETF:

- Dividends are automatically reinvested in the fund (€200 gross, not €148).

- You pay no taxes until the final sale.

- After 20 years: ~€28,700.

- At the time of sale, you pay 26% only on the total gain.

- Net final value: ~€27,200.

Difference: ~€2,200 more (almost 9% additional return) simply for choosing accumulation. This is the power of Tax Deferral: paying taxes at the end allows compound interest to work on the gross capital.

If during these 20 years you need €1,000 in liquidity, with the accumulation ETF you sell shares for €1,000 and pay 26% only on the gain from that sale (e.g., if those shares have risen by 50%, you pay taxes on €333 = €87 in taxes). With the distribution ETF, you would have already paid 26% on all dividends received up until that point.

Chapter 5: The Real Cost (TER and Tracking Difference)

How much does an ETF cost?

Everyone looks at the TER (Total Expense Ratio).

It's the annual management cost automatically deducted from the fund. Today, a good global equity ETF that tracks market cap costs between 0.12% and 0.20%. Factor ETFs (Value, Momentum, Quality) can cost 0.25%-0.30% due to the more complex management.

But the TER is not everything. It's just the tip of the iceberg.

The Total Cost (TCO)

The real cost is called TCO (Total Cost of Ownership) and includes:

- Bid-Ask Spread: The difference between the purchase and sale price in the market. If the ETF is illiquid (traded infrequently), the spread is high, and you lose money immediately upon entry.

- Taxes: 26% on profits (in Italy).

- Hedging Cost: If you choose a "Hedged" ETF to eliminate currency risk, you pay an implicit cost (the difference between the interest rates of the two currencies) that can significantly erode returns.

- Tracking Difference (TD): The most insidious and important cost.

The Tracking Difference: The True Indicator

TD is the difference between the return of the ETF and the return of the Index it should replicate.

TD = ETF Return - Index Return

If the TER is 0.20% but the ETF is managed very well (perhaps through securities lending), the TD could be only -0.05%. Sometimes the TD is even positive (the ETF beats the index!).

Securities Lending

Securities lending is when the ETF temporarily lends the stocks it owns to other investors (e.g., short sellers) in exchange for a fee. This generates extra income for the ETF that improves the tracking difference, but it introduces a small counterparty risk.

For the novice: it's a common and generally safe practice that helps reduce ETF costs. It’s one of the reasons some ETFs have a better TD than their TER.

Paradox: An ETF with a TER of 0.30% and a TD of -0.1% is BETTER than an ETF with a TER of 0.10% and a TD of -0.5%. Why? A TD of -0.1% means the ETF only loses 0.1% per year compared to the index (very close), while a TD of -0.5% means it loses 0.5% per year (further away). A TD closer to zero (or positive) is always better.

Don't obsess over the TER. Look at the real Tracking Difference on sites like TrackingDifferences.com.

As they say in finance: "The TER is promised, the Tracking Difference is paid."

💸 Confronto Costi: ETF vs Fondo Attivo

Scopri quanti euro ti mangiano le commissioni nel lungo periodo.

Chapter 6: Size and Liquidity

Another crucial parameter for choosing an ETF is its size, measured in AUM (Assets Under Management).

Closure Risk:

If an ETF is too small (e.g. under €100 million), the issuer does not earn enough from fees and may decide to close it. If that happens, you will get your money back (you won't lose it), but it is a tax hassle (forced taxable event) and an operational inconvenience.

Rule: Look for ETFs with at least €500 million in AUM. Over €1 billion is ideal.

Liquidity:

Liquidity of the ETF (how much it trades on the stock market) is often confused with the liquidity of the underlying assets.

In reality, thanks to the "Creation/Redemption" mechanism managed by Market Makers, the liquidity of an ETF is equal to the liquidity of the securities it contains.

An ETF on the S&P 500 will always be liquid, even if it has traded zero shares today, because Apple and Microsoft stocks inside are very liquid.

So don't worry too much about daily volumes if the underlying is solid. Worry about the Spread (which Market Makers keep tight on large ETFs).

Chapter 7: What's Inside? (Equity)

ETFs can contain anything. The most common are Equity ETFs.

How are they classified?

Geographical

- Global: MSCI World (Developed Countries) or MSCI ACWI / FTSE All-World (Developed + Emerging). These are the foundation of the portfolio.

- Regional: S&P 500 (USA), Stoxx 600 (Europe), TOPIX (Japan), CAC 40 (France), MSCI EMU (Eurozone), Emerging Markets.

- Single Country: FTSE MIB (Italy), DAX (Germany).

Note: The TOPIX index is the main index of the Tokyo Stock Exchange, but it’s more common to see MSCI Japan as a reference for the Japanese equity market.

Sectoral

Technology, Healthcare, Energy, Banks...

Caution: Here you are making an active bet. You're saying, "I know technology will perform better than average." Chasing last year's hot sector is a great way to lose money.

For a passive portfolio, ignore sectoral ETFs. You already have Apple and Nvidia in the Global ETF.

Thematic

Robotics, Hydrogen, Cyber Security, Blockchain.

They are often expensive marketing traps (high TERs) launched at the peak of hype. They often perform worse than the market after launch. Absolute caution is advised.

Chapter 8: Bonds and Mixed Assets

Not just stocks. ETFs are also excellent for the defensive part. But beware of durations: as we saw in the Previous Pillar, overly long durations can lead to extreme volatility. Bond ETFs They allow you to have a basket of different bonds. If an issuer defaults, the impact is minimal thanks to diversification.

- Government Bonds: State securities (e.g., Eurozone Government Bonds). Safe.

- Corporate Bonds: Corporate bonds (Investment Grade = safe, High Yield = risky).

- Aggregate: A mix of the entire bond market (States + Companies). The "buy everything" solution for the lazy.

WARNING: Some government ETFs show hundreds or thousands of holdings on JustETF, but they actually concentrate their assets on 4-5 main countries. Always check the actual concentration (top 10 holdings) in addition to the total number of positions. An ETF with "1,000 bonds" might have 80% of its assets in Germany, France, Italy, Spain, and the Netherlands.

Multi-Asset ETFs (Lifestrategy) These are the "Pension Funds in a box." They already contain both stocks and bonds in fixed percentages (e.g., Vanguard Lifestrategy 60 or 80). They rebalance themselves every day. They cost very little (0.25%). For those who want to dedicate ZERO minutes to finance, they are the ultimate and perfect solution. You buy one instrument and you're done.

Chapter 9: The Selection Process

How do you choose the right ETF among the thousands available on Borsa Italiana?

Here’s the Ultimate Checklist to use on sites like JustETF or Morningstar:

-

Index:

Which index do you want to replicate? (E.g., I want the S&P 500). -

Accumulation:

Filter for "Accumulation" (for tax efficiency). -

Size:

Sort by "Fund Size" in descending order. Discard those under 500 Million. -

Cost (TER):

Look for the lowest, but don’t go crazy over a 0.02% difference. -

Age:

Avoid ETFs that were launched yesterday. It's better if they have at least 3-5 years of history (to check the Tracking Difference). -

Replication:

Preference for Physical, but Synthetic is okay for the USA (if you know why). -

Currency:

The fund's currency (USD or EUR) does NOT impact currency risk (which depends on the stocks inside). But for accounting convenience, ETFs denominated in EUR on Borsa Italiana are the standard.

Practical example: I look for S&P 500 -> Accumulation -> >1 Billion AUM -> low TER -> iShares Core S&P 500 or Vanguard S&P 500. Done.

Chapter 10: Leveraged ETFs and Volatility Drag

There are ETFs that promise to multiply daily returns (e.g. "Lev 2x" or "Lev 3x").

They seem like the Holy Grail: if the index goes up by 10%, I gain 30%!

In reality, they are extremely dangerous tools for the long term due to a mathematical phenomenon called Volatility Drag (or Decay).

The Mechanism: Daily Reset

These ETFs reset their leverage every day. They must guarantee the multiple of the daily performance, not the annual one.

This creates devastating side effects in sideways or volatile markets.

The Mathematical Example

Imagine an index worth 100.

-

Day 1:

The index loses 10%. It goes to 90.- Leveraged ETF loses 30%. It goes to 70.

-

Day 2:

The index gains 11.1% (returns to 100).- Leveraged ETF gains 33.3% (3 * 11.1%).

Final Result:

- Index: Returned to 100 (Parity).

- Leveraged ETF: 70 * 1.333 = 93.3.

You’ve lost almost 7% while the index remained unchanged!